As I sit here writing this, I’m tired. But we’ll get to why so in a bit.

{Editor’s note: This lengthy post may include some crude humour, snark, swears, realism but ultimately is written with love, passion and from a place of hope. Don’t take it personally}

Introduction

I first discovered VR in the ’90s having tried a Virtuality machine at London Trocadero Centre, playing Dactyl Nightmare for a pricey sum. It gave me that first taste of virtual worlds and what could be possible, once the computing power available had improved and the features and capabilities of the technology alongside it. At the time it mostly gave me a headache and a funny feeling in my stomach.

Fast-forward to 2013 and joining a company that would go on to become a leading force in the UK for immersive content creation, the Oculus Rift DK1 KickStarter backer rewards appeared one day in the studio, re-igniting that passion for VR, now that it was more capable, cheaper and easier to create content for (as we all know it was still rough af at the time but still…)

I’ve written A LOT OF WORDS elsewhere already on this subject and already a series of thoughts after 9 years but blah blah blah here’s some more looking back more at the industry rather than my experiences.

As a scene-setter, let it be clear I LOVE VR! I want it to go mainstream, I love demoing and introducing it to new people but there are still many problems that need addressing…

Hardware

Back at the start of this current wave of VR, headsets were 3DoF and tethered. Motion controls were either custom-jobs or non-existent. The development environments were unstable but still, it was awesome.

3DoF quickly became 6DoF and motion controls emerged and gave us hands, whilst the length of the tether determined how much freedom of movement we had. This was the first great leap.

The next leap came in the form of standalone full 6DoF VR headsets, with inside-out tracking; whilst now reliant upon [specialist] mobile chipsets for processing power, many of the friction points were removed or at least reduced enough to move a step towards greater adoption.

Since then though, roughly 5 five years since 2018 when the first Oculus Santa Cruz dev kits were available, things have stagnated somewhat, at least in terms of leaps anyway. I think we’re due another leap soon but not seeing it within the current known line-up of devices for H2'23 or H1'24.

Yes there have been a number of necessary incremental upgrades and updates to various components, but even the sum of all these parts doesn’t really equal a leap per se, in my mind at least.

Processors have gotten faster and more capable; screens have increased in resolution; lenses have gotten thinner; devices have gotten lighter overall (mostly); form-factors are getting less bulky and dorky — but all of these are steps, not leaps. Yes the Bigscreen Beyond is flippin’ tiny and awesome but it’s a culmination of some of the above elements hyper-personalised for a niche user-base (which is also fine) (and is still tethered).

Cost has massively dropped since 2013, with users no longer needing high-end gaming PCs to attach a headset to. It is interesting to consistently see standalone VR owners posting in various groups about VR PC specs and whether they are good enough to run PC VR. There is a desire to spend more than the lower cost of a stock standalone headset, especially when you look at some of the battery, strap and audio accessories some users attach, adding £100s of extra to the cost. Much of this is a reflection on the corners being cut to reduce costs of manufacturing and production.

At the other end of the scale is the highest of high-end VR, typically PC VR. Manufacturers such as Varjo are pushing the boundaries of the technology, and our wallets, with fantastical devices that are beyond the average consumer. Their XR-1 headset showed how MR should be done with hand occlusion and high resolution passthrough video. No doubt new devices will continue to up the ante of where things can go.

Talking of cost, let’s skip over Google Cardboard, entering the market at the other end. Yes there were some benefits, like being affordable and allowing wider demographics a chance to own and develop for VR but ultimately, the experience and impact overall was so bad it really hurt adoption for many years afterwards. Still to this day, has been some peoples’ only experience of “VR”, having put them off for life.

Mixed Reality

Some would argue this is the next big leap for VR headsets… to a degree it is; this new ability to flip between AR and VR as promised. Maybe I’ve just gotten too used to hardware advances that it didn’t wow me much, or the killer app / use case hasn’t been shown yet.

All current & next-gen standalone VR headsets now offer full colour passthrough as a means to Mixed Reality (MR). Not that MR, the one Microsoft tried to coin, or that other one, used to describe marketing videos where you could see the person in VR from a 3rd-person viewpoint to make far more engrossing videos to watch… Now we’re talking about seeing the real world around us, rather than being “isolated” in fully immersive virtual environments, bringing 3D content into the mix and having it spatially aware within physical spaces.

At a simple level this is doing what HoloLens and Magic Leap offered, albeit with video passthrough rather than visors and waveguides, enabling wider FoV, greater colour contrast (& black!) at lower costs. All great stuff. But what do we do with it?

Visor passthrough taught a number of people that this form was hard and expensive (excluding the low-cost TiltFive method). Video passthrough has a number of benefits but is still hard and may not fix some of the new issues created, such as warping of the video around hands etc we see currently with all devices.

Developers have had 10+ years to explore, experiment and play with VR design, interaction and development to understand what does, and doesn’t work. I feel we’re very much back at the start of a cycle with MR today but without many of the earlier pioneers to play with the possible.

I fully appreciate and 100% support the fact that seeing the world around you still whilst wearing a VR headset is a lot less scary to many users, a previous barrier to adoption for many, but why do we need it?

There’s that word that’s always there with VR; WHY?

MR feels like a new capability, a bit like AR, that is still searching for a valid use case to make it really take hold and catch-on. Hardware platforms are all pushing MR capabilities to varying degrees of technical ability but are we really seeing consumer demand for it? I’ve seen a lot of pitches for MR titles of late and only a small handful really stood out as being worthy. Shout out to Demeo local co-op MR mode, Track Craft and Laser Dance.

Platforms need to do more with funding and supporting more developer experimentation to explore MR possibilities, much like early VR was — this time there’s a much larger userbase and far more knowledgable devs with much more stable environments to work in, so it seems a much lower risk this time around. But where is the money?

Once the Apple Vision Pro launches with a range of amazing app experiences (TBC) and we’ve all fully switched to calling everything Spatial Computing, I could end up looking very silly at that point but only time can tell. Apple’s vision *sic seems very different to what we have come to expect, very much relying on 2D apps and planes of positioning rather than the fully immersive worlds we are more used to. Like many advances made, today’s devices feel like prototypes of what could be achieved in years to come once we work out how to reduce the form factor and goofy-looking nature of headsets today.

Similarly there are a number of working prototypes being built that actually allow us to test out ideas hoiked across LinkedIn over the years as concepts using mobile AR or pre-rendered scenes. However cool having floating video panels and live weather updates pinned to our walls is, am looking forward to the real wild experiments that push beyond the obvious.

Terminology

VR, AR, MR, XR… those in the industry argue and debate constantly what each term means, where the boundaries are and so on until we’re all blue in the face and no where nearer an answer or a definition. However outside of the industry, the mainstream media (when they actually cover it), the end-users, everyone else doesn’t care! Typically everything will be called VR, or confused between AR and VR and now we’re trying to add MR and XR in there. MR has already had three definitions/uses and the industry will debate ’til the cows come home whether it’s xR, XR for all of the above, or eXtended Reality… it really doesn’t matter. Apple will be launching the Vision Pro next year and using the term Spatial Computing (originally from Magic Leap ¯\_(ツ)_/¯) so that’s what we’ll all be calling it from then on anyways. Everyone else just calls devices, no matter what they are, “them goggles”, and I’ve come to learn to live with that.

Input

VR is all about incorporating as many senses as possible to enable immersion, which once achieved can allow a user to feel presence. Beyond what we’re making peoples’ eyes see, what they touch and feel is just as important.

From Xbox gamepads to Razor Hydras to PS Moves to Vive Wands, Oculus Touch, Valve Knuckles, Sense Gloves, PS VR2 Sense to throwing all that out and just tracking our hands with Leap Motion, Ultra Haptics or inside out tracking cameras, input is still a big sprawling mess of development.

Thankfully at least from a motion-tracked controller aspect we’ve settled on a mostly standardised set of triggers, grips and buttons across platforms but we’re about to enter a phase where many new users enter, now that Apple has, only ever knowing hand-tracking.

Hand-tracking is great again for people who are fearful of tech (and especially gamepads) as it removes another potential barrier to adoption. We all know how to use our hands right? Although as anyone who developed for the first HoloLens recalls, trying to get a human to reliably repeat a L>pinch gesture is near impossible after being shown how.

But we lose all the haptics with hand-tracking and there’s nothing out there that really replaces that, at least without adding great cost or friction for setup to replicate elements of physical touch, mostly quite poorly. And hand-tracking itself, although getting more robust and reliable with each iteration of firmwares and SDKs, still feels a bit inaccurate or off at times or requires specific lighting conditions, adding back to the friction of setup.

There’s been rumours of various device manufacturers prepping controller-free SKUs over the years but H1'24 will see Apple be the first to do so, when they ship Vision Pro without controllers and apparently little inclination to enable support for them in the future. Again, time will tell if this is a wise decision I guess. In the meantime there’s a lot of developers frantically working out if their controller-based systems and apps will work without them.

Software

Content* is king! Retention is queen? Whatever that means by todays standards, a large library to choose from is only as useful as the people sticking around to use applications and experiences repeatedly. Or is it just a sign of maturity of the marketplace if people are buying titles and never playing them, a la Steam piles of shame?

Whilst the development standards (OpenXR) encourage and enable a more open approach to distribution, today we find ourselves with numerous walled garden app stores for VR, all taking their 30% cut of revenue from developers of an emerging marketplace, where every penny of sales revenue counts. I’m all for a new model where platforms only take a %-cut after a title has made x-amount of revenue, or it scales more in the favour of the developers success. 30% of sweet FA is not a lot to fight over anyway.

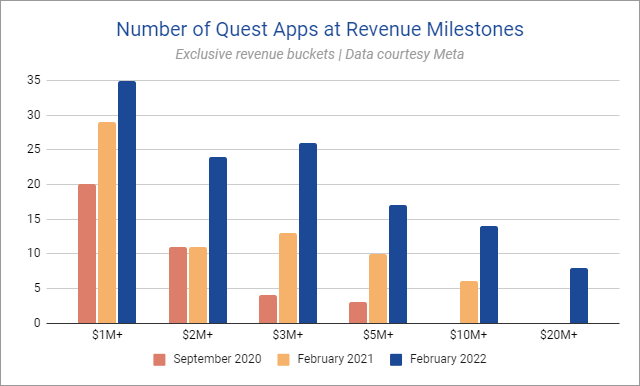

Meta got it right though with the pricing of the Quest to “stack them high, price them low” to create the largest marketplace for developers to find success** within, with some fairly good and some fantastic stats of title revenues across the years for a lucky few studios. Other marketplaces have failed to capitalise on potential install base opportunities, through pricing and/or funding decisions, or regional availability. But the suggested 15–20M+ marketsize of Quest users is gatekeepered off to many developers, pushed to AppLab without the luxury of discoverability or marketing to capitalise on those hungry for more.

Continuously over these 10 years has been the need for funding and support for developers and studios, which has ebbed and flowed, flooded and been in drought in equal measure. A common misunderstanding has been the cost of development from all sides of the table, and at the end of the process, of what it takes to make a really good experience. Similarly what it takes to make really good VR, or something that feels great in VR.

Time/budget/effort is always against every development team when end users are demanding more, often seeing them willing to port flat experiences into VR with rudimentary success or impact, worsening the situation or causing more friction to adoption. (On the other hand there are some great flat-to-VR modders who have done amazing jobs with a few titles making them huge fun to play and appealing to new audiences.)

One big area of debate and contention for software (well and hardware) is whether PC VR is dead or not. It’s not, it’s just resting. Again looking at market sizes, with approx’ 4M VR devices connected to PCs (gathered through Steam Hardware Surveys), that’s a smaller market than standalone (Quest, 20M+) and PS VR (6M+) (PC VR 2 numbers are unknown currently) and with dev costs rising and funding drying up, one can understand why many studios focus on where they could potentially maximise their chances of revenues being returned.

There are some titles that have sold more copies on PC VR than standalone, due to the nature of the title and their audience expectations but these are few and far between. It can be done but it’s certainly not the norm. Either camp (standalone or PC VR users) are united in crying out for more though. Depending upon studio expectations and development cost, PC VR is still a viable place to release titles and with marketplaces like Viveport and Infinity offering more carefully human-curated storefronts, there is a place for great titles to shine & standout amongst a tonne of shovelware and crap.

Like demands for more titles however, its clear the standard purchaser behaviour of waiting for sales is the same across standalone and PC VR; Winter (holiday) and Summer (& Spring, Autumn etc) Sales on all storefronts boost numbers of units shifted considerably compared to non-sale times (with Christmas Day / Boxing Day still typically being the main sales point for a lot of titles). Whilst overall sales numbers are shown to be down in 2023, will be interesting to see what happens when hardware refreshes and improved specs hit the market and whether this needle moves or not***.

I think things that have hurt the competition to Meta Quest though is the availability of titles on other stores, device region availability itself or just simply cost of hardware. Key titles are missing from competitor stores for a variety of reasons but ultimately either price being too high or the device not being available in America (usually 60% of a VR title revenue) has stiffed them from providing a viable alternative place for studios to be successful on.

(***NB. I started writing this before Quest 3 released but Meta never share numbers anyway)

User Experience

I think one of the biggest barriers to adoption still prevalent today is the overall user experience of putting a headset and launching a title.

There’s still a lot of faff involved with using VR although admittedly, there have been many improvements these past few months to make things a bit easier.

Thankfully most of the earlier friction around setting up VR has been eliminated with the introduction of standalone devices, no longer needing external sensors, tethers and running multiple apps and setup on a PC. (Of course PC VR is still a thing that exists so these friction points still exist if that’s your flavour of choice, especially if you don’t have a dedicated setup and just get it out every now and then.)

The most recent standalone devices with depth sensors, or even the Sony PlayStation VR 2, allows for room scanning and mesh generation to automagically create a guardian space for the user, removing another setup friction point. Thankfully these can still be edited and finessed by the user.

Even still, with standalone there’s regular app and OS updates that need to be applied in-headset, which you can’t do from the companion apps. If you add multiplayer to the mix, then creating a room, or a party, getting your friends, or foes, together and joining the same lobby for a particular game is still a pretty big ballache.

It is getting better with more being able to be done from the mobile companion apps and deeplinks you can share with friends outside of VR (if the developer has implemented them) but there’s still work to be done.

Of course in early 2024 Apple will release the Vision Pro and whilst there’s been a lot of chatter about the development side of things, we still don’t know a great deal about the actual user experience and how updates and interactions outside of the device will be handled until it’s launched. IF there’s one thing Apple prides itself on, and others celebrate it for, is user experience so will be interesting to see how they handle things.

Gaming

Once the main focus of the rebirth of VR, rightly or wrongly, gaming and targeting gamers, beyond just the VR devs supporting each other has had its ups and downs. Look at any mainstream gaming website article about a VR title or device, and many of the comments underneath will be very anti-VR as a whole. This hasn’t really changed in 10 years with all the advancements to the tech, the increased reach and availability and the range of experiences available. Some gamers just do not want VR, and that’s OK. I think we need to learn to live with the fact that whilst we are all super positive and supportive of VR and wanting it to grow, there is a large portion of people who simply do not give a shit.

VR gaming now suffers the same fate as flat gaming; gamers just moaning about lack of content, graphics not being shiny enough, whether a title is worth x-amount, waiting for a heavily discounted sale before purchasing, stroppy demands, thinking adding VR is just ticking a box in Unity and oh so many kids in multiplayer. But does that mean it’s gone mainstream?

*Content [Creators]

It wasn’t really until speaking with Jörg Tittel recently that I realised content is a bad word for experiences designed to make you think, react and feel. Content is to be consumed, chewed up and spat (or shat) out and this isn’t a valid term for the experiences we want in VR. It also created a minor existential crisis internally for me, having had the word in my job title; to be fair this was further exacerbated by constantly being emailed about opportunities to work with YouTubers and influencers and their content, or sponsoring event promos, completely unrelated to what I was doing.

Anyway, over the years the rise of the VR streamer, Let’s Player, YouTuber, influencer, content creator, whatever you want to label them/yourself as, has been a boon and a curse in many ways.

From the first time the good house of SundayVR opened its doors 10 years ago to a wave of excited DK1 owners by CymaticBruce, the OG VR streamer built-up a community around showcasing the latest and greatest demos and experiences. Fast-forward to today, I’m currently tracking 200+ VR streamers on my Twitter list (of those on Twitter anyway) from those with a few subs to those in the thousands. I don’t think any dedicated-to-VR have hit 1M+ subs yet but some are getting close…

As with all influencers there’s been a fair bit of discourse over the years about their value, influence and whether or not they are paid shills by platforms etc. As with all things consumer, they have become part of the marketing machine and are useful but perhaps not as valuable as some will have you believe (or what they want to charge you for coverage*). It’s good to see a continuously growing number still getting excited by VR but some real in-depth knowledge and discourse amongst more of them would be great to see too. To be fair, a number are now using their years of experience and play time across thousands of titles to work directly with studios and push platforms to improve features necessary to really showcase the feeling of playing VR.

*I am all for appropriately paying people for their creative time, work and effort

Grifters

You know who they are. You know where they hang out. They can be spotted with their ever-changing job titles incorporating the latest buzzword, whether it’s VR, AI, NFTs, Web3, GenAI, metaverse etc…

Do yourselves a favour, do due diligence on these people if considering paying them for insights or costly consultancy. Avoid feeding their narcissistic need for attention and clout.

Enterprise

I spent 10 years educating and evangelising the transparent and honest truth about how immersive technologies could potentially benefit enterprises, either internally or externally and it got tiring saying the same thing, to the same types of people, over and over and over.

Cardboard hurt adoption (as mentioned above) and it hurt the ability to demo VR to people at events for sure. It also hurt expectations of what was possible, i.e. just 360º video without experiencing full VR and real possibilities.

But organisations are usually slow lumbering machines, often with people happy with the norm, fearful of change and looking to maintain an easy life and pay-cheque. VR disrupts that and a lot of pushback happens as a result. Even when a pilot or prototype is deployed, and successful, there’s still so many barriers to wider adoption, it sucks the life and time out of smaller studios trying to deal with these across multiple projects. From security and IT, to departments that feel they should be the ones innovating with VR instead, stakeholder engagement and getting everyone onboard early on to avoid blockers later on is a full time job, one that unfortunately has to come at the cost and detriment of the studio, not the organisation.

There are those though who are an absolute delight to work with, who are open-minded to change, innovation, adoption of new ways of working, learning and collaborating, to make everyone more efficient and improved human beings. Thankfully the majority of those I’ve had experience working with fall into this latter camp. Look for those organisations and learn to spot early on the other type, knowing when to walk away until they are ready (if ever). But business organisations are careful and cautious, flashy sales promises and vague, unsubstaniated numbers don’t rub on procurement departments.

Honestly, maybe some doors have closed there, maybe for good? The pandemic and lockdown gave VR a chance to shine, to prove it’s value to businesses looking for remote working tools, or today supporting hybrid solutions but did it? I don’t think it took off or had a boom like many were hoping or predicting. For sure, at the start of that period of time, there was a shortage of components and manufacturing was impacted, meaning organisations couldn’t get devices at volume anyway. But then availability improved but now many are back to the office, has that impact lasted?

There has been a rise in enterprise software storefronts, for organisations wanting access to more work-orientated immersive experiences and tools beyond the single, bespoke application they’ve built, or had built for them. How successful these are is anyones guess at this point with no data being shared but choice and expansion of hardware fleet usage is always good.

Another rise has been the one-off corporate training day session, run by experienced providers, rather than having hardware in-house. Companies like VirtualUmbrella regularly post updates of setting up 200–300 VR HMDs for these purposes, hired by organisations to run training sessions with specific applications and outcomes. So even if it’s a struggle to get traction internally, there’s valid use cases externally.

{It should also be noted that cost of living, global inflation, interest rates, UK-specific government cock-ups impacting credit and investment, Brexit and willingness to spend certainly hasn’t helped the situation either}

The Metaverse

The M-word… the next big thing that was massively overhyped, misunderstood and mis-labelled by many organisations hoping to cash-in before the bubble burst… urgh. Oops, too late I guess.

To me, the metaverse will be the next evolution of the internet, plain and simple. But we’ll just carry on calling it the internet. Much like information superhighway or cyberspace, this is just another silly name no-one will use in the long run.

But let’s be clear, your app or platform, even if it lets external UGC data in, is still just that, an app or platform. There’s 150+ social-based apps claiming to be the metaverse. No one company will make or own the metaverse, it will be an emerging technology standard that’s open and interoperable, and it is not here yet.

The only app we’ll be using for the metaverse is a future version of your web browser, on your device of choice.

Funding

Developers need to be able to eat and support themselves and their families whilst making things, nothing new there. However with emerging technologies there are many more inherent risks associated with building for them. Over the years as the hype has boomed and bust, funding was more or less readily available but generally unevenly distributed.

Studios could get rich *sic quick by focusing on areas that were popular in the short term but that left them vulnerable when attention and desire waned, i.e. marketing VR and AR experiences. Platforms were keen to embrace and encourage devs to get involved and early on, support via dev kits and grant funds were more easily accessible. However shifting winds, people and directions left a number of studios suddenly without financial support or even contacts, not to mention those whose concepts inspired new platform features, killing their USP.

When building new marketplaces for new devices, it should seem logical to support developers to encourage them to come onboard and support emerging platforms. Especially when unit sales are unknown or starting from scratch, where ROI is unproven, development costs effort (time & money) and studios have to mitigate risk of involvement to do so.

Some studios and manufacturers see enterprise as the golden goose for funding options, as business = $$$ right? Wrong! You can’t just charge x3 the unit price or costly software licences and expect organisations to cough up large sums on untested technology or unproven outcomes.

Immersive artists are lured to festivals with promises of premieres and exclusive launches, exposure, fame and fortune. Sure, maybe if you are the lucky one who sells for a large stack of dirty oil money but most are left wondering how to feed the family with a laurel. Replicating a broken film model, without next-stage funding providers in place, creates a cycle of poorly-funded prototypes that aren’t technically performant, with no means of wider distribution beyond that one inaccessible festival event.

I’ve said already above but as hardware manufacturers push MR onto end users, they need to be funding more experimentation and exploration so that developers can play and learn what does and doesn’t work, much like many did with VR in 2013 onwards. Otherwise we end up with generic internal demos and concepts that do not push creativity or possibilities beyond a safe, simple idea that fails to ignite any interest amongst consumers.

AI

A minefield of ethical and moral quandaries, AI is currently being pushed by tech bros with their usual distruption-first mindset. Why we’re targeting the least well paid and often most creative jobs with AI, rather than say, middle management, is beyond me. I’ll all for democratisation of creativity and allowing everyone to be able to build but until we have global UBI, AI is going to create more problems than it solves in the short-term IMHO. Similarly we need a number of efficiencies around consumption, like with blockchain, crypto-mining and cloud storage, so our technological paths don’t drive us to climate chaos (any more than we are already headed).

Summary

So why I am tired?

I’ve spent 10 years pushing for adoption, doing many events to enable public access to xR, enterprise education workshops and talks, panels and whatnot to honestly and transparently talk about the potential benefits and use cases of the technology, as well as highlight current pitfalls and shortcomings.

I’ve worked on both sides of the table, in software and hardware, in development and publishing, and I’ve peeked behind a few curtains. I’ve debated over terminologies and tried to avoid hype and conjecture, generally ignoring predictions, rumours and speculation until prototypes, dev kits and tangible tools have been in my or developers hands.

VR certainly is not dead and I am still very positive about the future prospects, but after 10 years it seems very much still a “yeah but in 3-5 years time…” technology, that still needs to solve a lot of hard problems and barriers to adoption before it goes mainstream.

I’ve rolled my eyes every time someone said “VR is dead!” but looking back over the past 10 years and where we are today, we have to be truthful about what alive means.

I’ve previously controlled external comms and how we spoke about technology to clients for many years within a studio, making sure we were open, honest and transparent about the potential benefits and use cases, whilst also highlighting the pitfalls and shortcomings. All the above may read as me being cynical but ultimately it’s realistic, truthful & valid IMHO.

I’m not dead, I’m tired, I’m just resting. I’m looking forward to stepping back a bit and enjoying what comes as a consumer, with a keen eye and ear out for developments as an interest I can maintain my passion in.

No doubt I will soon be back supporting studios making immersive experiences through work and helping them find success as creators, I love it too much. Similarly continuing to share relevant and important news and updates from all platforms, studios and the wider industry sectors.

Be kind and be excellent to each other. Build awesome stuff and have fun. Be aware of those who do not have your best interests at heart. Be strong.